CFO Biweekly: 2026/6/18

When "Cheap" Becomes the Most Expensive Signal — The Market Assumptions of June 2026 Face a Triple Test

If your hedging costs came in lower this year than last, don’t be too quick to drop that number into the “good news” column of the governance report. Odds are it wasn’t your negotiating; instead, it was the contract rolling over in exactly the right month.

*This article was written on June 14th, beware of the difference in numbers today

The $300,000 I saved the company on hedging may be the most expensive decision I make this quarter.

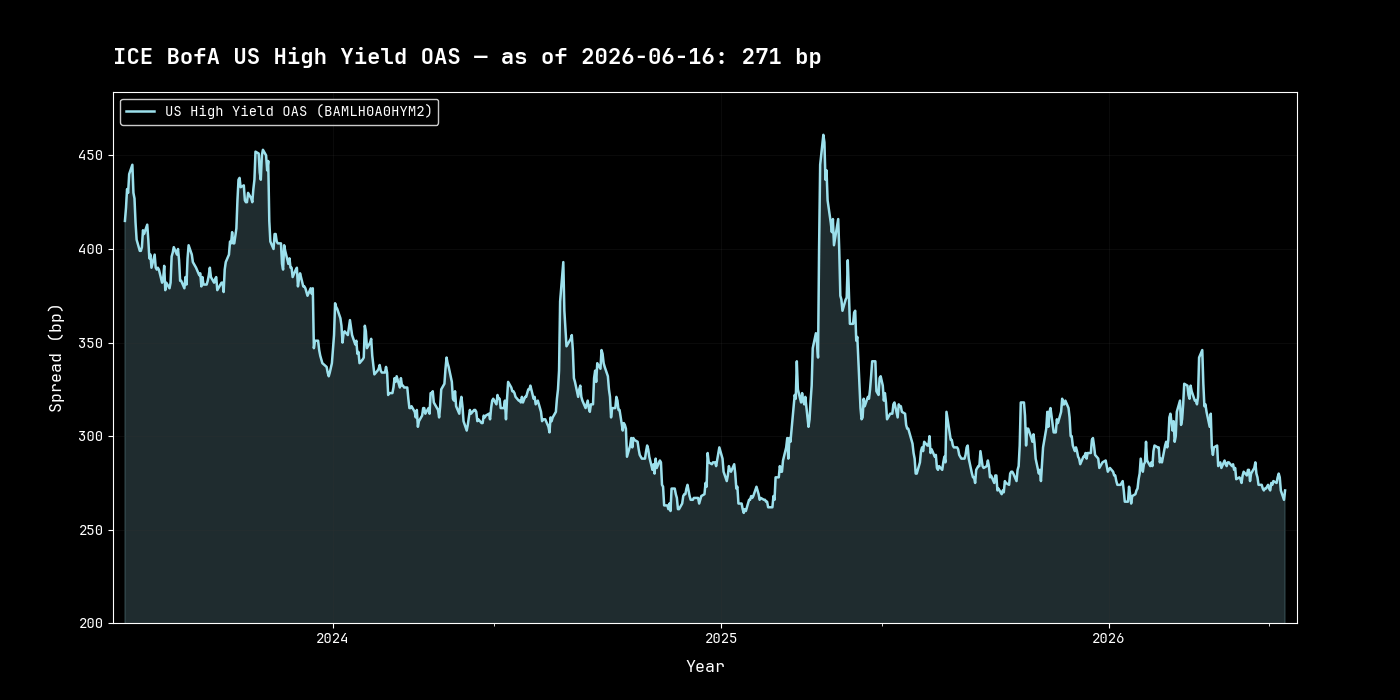

HY-IG spread: 202 basis points, that is 148 bps inside the ten-year average. Same week, the energy hedge quote came in 20% cheaper than a year ago. The same set of assumptions generated both numbers.

The renewal quote for the hedge portfolio landed on my desk this week, 20% below last year’s level. Treasury has already penciled the figure into next month’s draft governance report, probably under a heading like “Hedging cost optimization: ~$300k annual saving.”

My first thought wasn’t we saved. It was why is it cheaper?

The answer sits on a completely unrelated chart. The HY-IG credit spread: 202 bps (ICE BofA, June 2026), a full 148 bps inside the ten-year average of 350 bps. Same week, Brent crude dropped more than 4% in a single session and roughly 6% for the week after an official remarked there is “an 80% probability of a near-term Hormuz deal” (CNBC, June 12, 2026). Also the same week, the ECB revised its 2026 eurozone inflation forecast up to 3.0%, explicitly premised on a “persistent” Middle East conflict (ECB Monetary Policy Statement, June 11, 2026).

Three stories that look unrelated. But the 20% discount on that hedging quote runs on the same input as all three.

A hedge price is never calculated in isolation. It moves with the entire volatility curve, and that curve was pushed lower this week by two forces at once: credit markets compressing the geopolitical risk premium to 202 bps, and crude markets pricing the same headline category as a 4% intraday drop with no follow-through. Curve gets crushed; our collar premium gets cheaper along with it.

Run the numbers. Assume a $100 million energy exposure, hedged last year with a collar structure at a premium of 1.5% of notional, or $1.5 million. Same structure this year, quoted at 1.2%, or $1.2 million. The $300,000 difference is about to be reported as this month’s win.

But the model that produced the 202 bps spread and the model that priced the collar 20% cheaper are both fed the same assumption: the market now thinks it’s calm. If that assumption is wrong—if the ECB’s “persistent conflict” script ends up being a lot closer to reality than the Hormuz “80% solved” story—then the $300,000 was never really saved. It was just a risk that used to be priced, moved from a budgeted, scrutinized line called “hedging cost” to an unmonitored corner of the balance sheet called “unhedged exposure.”

Hedging costs falling doesn’t mean risk is falling. It means the market has decided, for now, not to charge for that risk. And the ledger will never record the words “the market decided.”

Take it one layer deeper. The reason this quote arrived now has nothing to do with the risk itself. It’s because our energy hedge happens to renew in June. If the contract calendar had landed in March—amid the Hormuz shock, with spreads still near their long-run average, this same renewal would have hit the high end of last year’s curve. The premium would have been more expensive. The governance report would have read “hedging costs rising.” Same company. Same risk. Same compressed assumptions. Two completely different stories, depending entirely on which month the contract expires. That’s not better or worse risk management relative to peers. That’s calendar luck.

What makes it worse is that even the board won’t see it. The hedge quote sits with the treasury team. The credit spread sits with corporate finance. Those two pieces of paper never appear in the same board pack. The only person who can hold “the $300,000 we saved has something to do with the fact that the contract expires in June” in one place is whoever sits at the intersection of the two lines, a job description that happens to match that of the CFO.

There’s another decision on my desk this week: the $250 million HY-B refinancing we had put on hold. Last week’s judgment was “wait until all three triggers align.” This week adds a new variable: a spread level of 202 bps might not be a waypoint. It might be the best price available during this stretch of “the market isn’t charging for the risk yet.”

This week’s call: we are leaning toward pulling the trigger on the $250 million refinancing now rather than waiting.

Subscribe to read the full analysis: (1)The three triggers for launching the refi; (2)The opportunity cost math of waiting vs. moving now (including my own probability weights, which invert the market’s); (3)Three indicators to watch next week, with specific action thresholds.